You cannot afford your whole life insurance premium anymore. Maybe income dropped, retirement hit earlier than expected, or priorities shifted. You are tempted to just stop paying and let the policy lapse. Before you do that, you need to know one thing.

What most policyholders do not realize is that their whole life policy already contains a built-in exit option that does not require them to give up everything. It is called reduced paid up insurance, and it is written into nearly every whole life contract.

What Is Reduced Paid Up Insurance?

Reduced paid up insurance is a nonforfeiture option that converts your whole life policy into a smaller, fully paid-up policy with no further premiums required. Your accumulated cash value acts as a single lump-sum payment to purchase a guaranteed death benefit for the rest of your life.

In plain terms: you stop paying, you keep coverage, and you do not lose your cash value. The trade-off is that your death benefit gets smaller. How much smaller depends on how much cash value you have built up and how old you are at the time of conversion.

This option is available in almost every whole life insurance policy. According to Insurance and Estates’ 2026 RPU guide, eligibility typically requires the policy to have been in force for at least three years and to have accumulated sufficient cash value. Some insurers require longer, so checking your specific contract matters.

How Does Reduced Paid Up Life Insurance Actually Work?

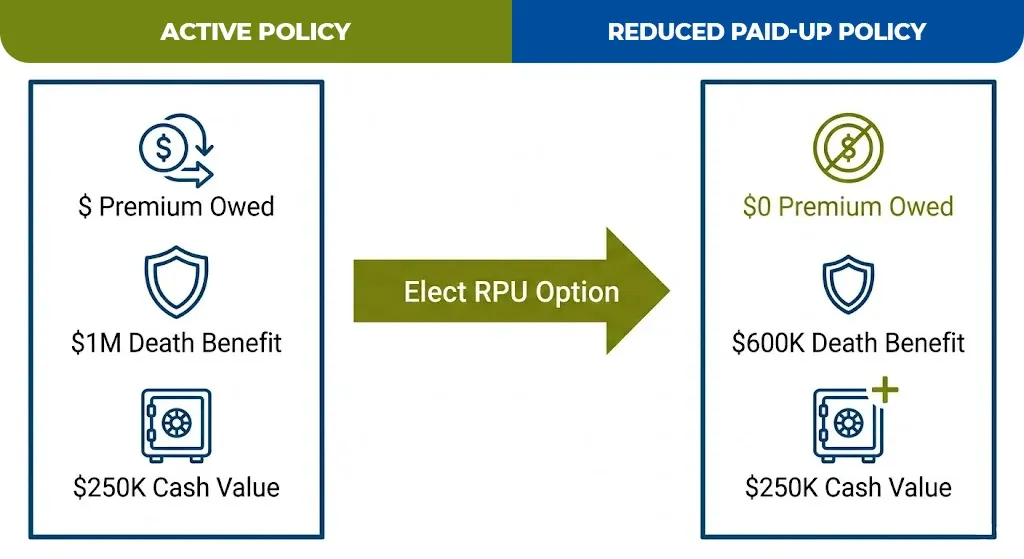

When you elect the reduced paid up option, the insurer uses your current cash surrender value to calculate the largest death benefit it can guarantee for life without any future premiums.

Here is a real example that makes this concrete.

Vivian has a whole life policy with a $1 million death benefit and $250,000 in accumulated cash value. She elects the reduced paid up nonforfeiture option. After conversion, her death benefit becomes $600,000, she owes no more premiums, her cash value remains at $250,000 and continues to grow, and she can still take policy loans against that value. That example comes directly from The Insurance Pro Blog’s 2026 nonforfeiture analysis.

The converted policy is still a whole life policy. It retains guaranteed interest on cash value, eligibility for dividends, and the ability to take policy loans. The only thing that changed is the death benefit amount and the premium obligation.

What Does Reduced Paid Up Mean for Your Cash Value and Death Benefit?

Your cash value does not disappear. It stays in the policy and continues earning guaranteed interest and, in participating policies, dividends.

Your death benefit does get reduced, and the calculation is based on your age at conversion and your policy’s accumulated cash value. A policyholder who converts at age 55 with more cash value will retain a larger death benefit than someone who converts at 65 with less. The insurer is essentially treating your cash value as a one-time, single premium to purchase a smaller permanent policy.

One detail that surprises many people: as dividends accumulate post-conversion and are used to purchase paid-up additions, the reduced death benefit can actually grow back over time. According to Insurance and Estates, over a 10 to 20 year period, dividend-funded paid-up additions can recover a meaningful portion of the death benefit that was reduced at the time of election.

One more important note: once you elect this option, it is permanent. McFie Insurance’s 2026 RPU breakdown is direct on this point: you cannot reverse the conversion and return to your original policy, even if your financial situation improves later.

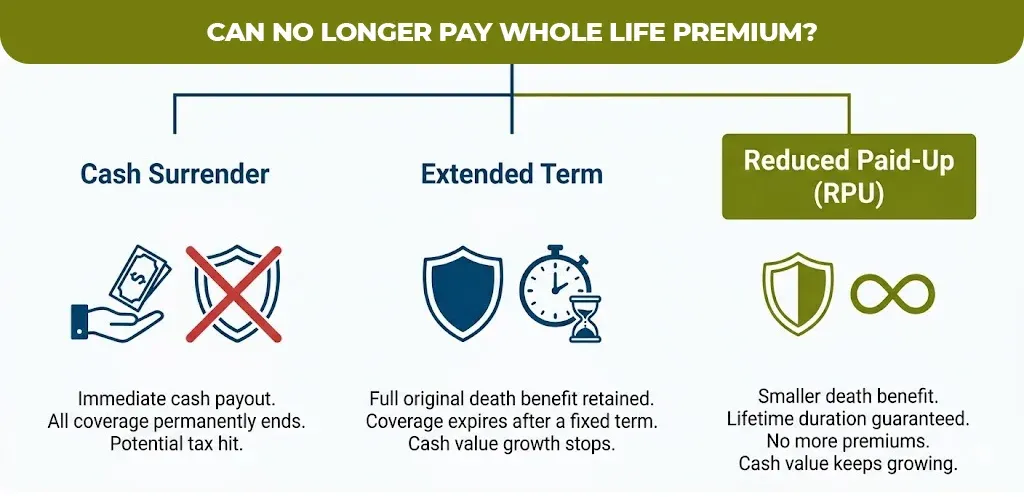

Reduced Paid Up vs. Other Nonforfeiture Options: A Clear Comparison

Every whole life policy comes with at least three nonforfeiture options. Choosing the wrong one for your situation is easy to do under financial stress. Here is how they compare.

| Option | What You Get | What You Give Up | Coverage Duration |

| Reduced Paid Up (RPU) | Smaller death benefit, no more premiums, cash value grows | Lower death benefit than original | Lifetime |

| Extended Term Insurance | Full original death benefit, no more premiums | Cash value stops growing, no dividends, no loans | Limited term only |

| Cash Surrender | Lump sum of cash value minus fees | All coverage ends, possible tax on gains | None |

The critical distinction is duration and what happens to cash value afterward.

Extended term gives you the full death benefit but only for a fixed number of years. After that period ends, coverage disappears completely. Cash value does not grow, and you cannot borrow against the policy.

Cash surrender terminates everything. You get the cash, but you give up permanent coverage entirely and may owe ordinary income tax on any gains above your total premiums paid.

Reduced paid up is the only option that keeps lifetime coverage intact while also preserving cash value growth. According to LongTermCareDesk’s nonforfeiture comparison, reduced paid up insurance preserves the most permanent insurance protection of all standard nonforfeiture options.

Who Should Use the Reduced Paid Up Option (and Who Should Not)

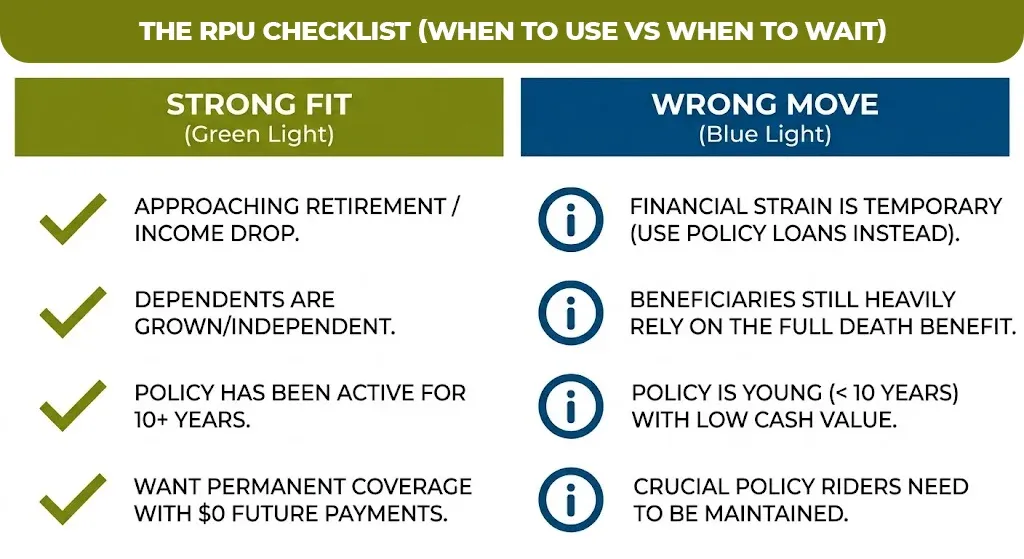

The reduced paid up option is the right call in specific situations. It is not a universal fix for every financial problem.

Reduced Paid Up Is A Strong Fit When

- You are retiring and your income is dropping, making the original premium unaffordable

- Your need for a large death benefit has genuinely decreased, such as when dependents are grown and financially independent

- You want to keep lifetime coverage without the burden of ongoing payments

- You have built substantial cash value over many years and want to preserve it

- You need to eliminate an expense without triggering a taxable event from surrendering

Reduced Paid Up Is The Wrong Move When

- Your financial difficulty is temporary. A policy loan or automatic premium loan feature may be a better bridge until cash flow recovers

- Your beneficiaries still depend heavily on the full death benefit

- You are early in the policy, typically under 10 years, and cash value is still low, which means the converted death benefit will be very small

- You have riders on your policy that are valuable to keep, since many riders do not carry over after conversion

McFie Insurance recommends allowing a whole life policy to build cash value for at least 10 to 15 years before seriously considering the RPU option, because conversion on a young policy produces a very small death benefit in return.

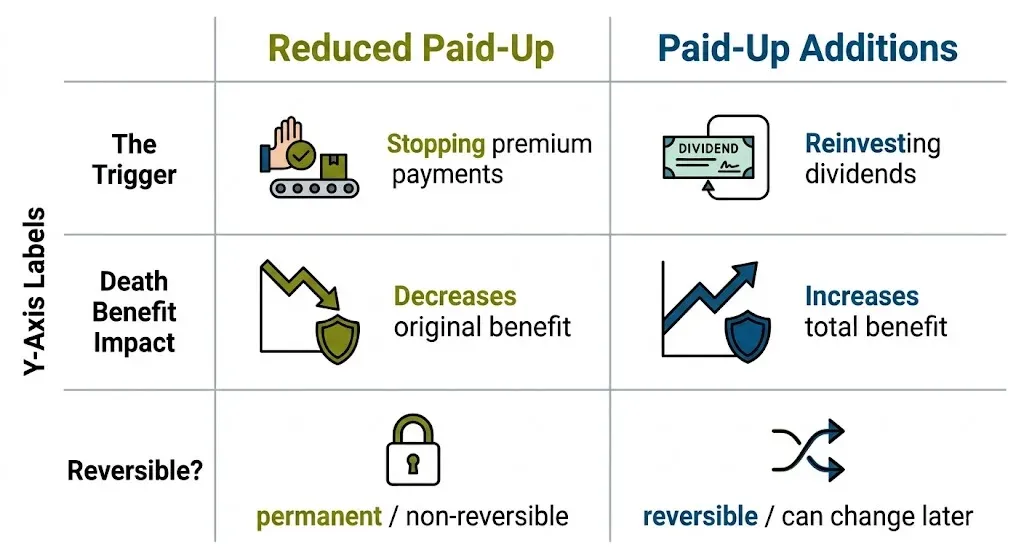

Reduced Paid Up vs. Paid-Up Additions: They Are Not the Same

This is a common source of confusion. Paid-up additions and the reduced paid up option both involve life insurance that requires no premiums, but they work in completely different ways.

| Feature | Reduced Paid Up (RPU) | Paid-Up Additions (PUAs) |

| What triggers it | Electing to stop premium payments | Using dividends to buy additional coverage |

| Effect on death benefit | Reduces it from the original amount | Increases it above the base amount |

| Cash value impact | Preserved and continues growing | Also grows, adds to overall cash value |

| When it applies | When you stop paying the base premium | During normal, ongoing policy participation |

| Reversible | No | Yes, dividends can be redirected |

Paid-up additions are a growth tool used during active policy participation. They use dividend payments to purchase small increments of additional whole life coverage, increasing both the death benefit and cash value over time.

The reduced paid up option is an exit strategy for premium payments. They are related in structure but serve entirely different purposes.

Thinking About Whether This Option Makes Sense for Your Policy?

If you are facing a situation where premiums are becoming a strain, or you are approaching retirement and wondering how to adjust your whole life policy without losing everything you built, reduced paid up insurance deserves a serious look before you make any other decision.

The right answer depends on your specific policy, how much cash value you have accumulated, your age, and what your beneficiaries still need from you. Those are not questions a general article can answer for your specific situation.

Mlife insurance works with policyholders at exactly this kind of crossroads. If you want a clear picture of what your policy options actually look like in numbers, not just concepts, that is a conversation worth having.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.