Shopping for life insurance without understanding what level actually means is how the families end up with a policy that will look affordable in year one and then it becomes difficult for the finances by year eight.

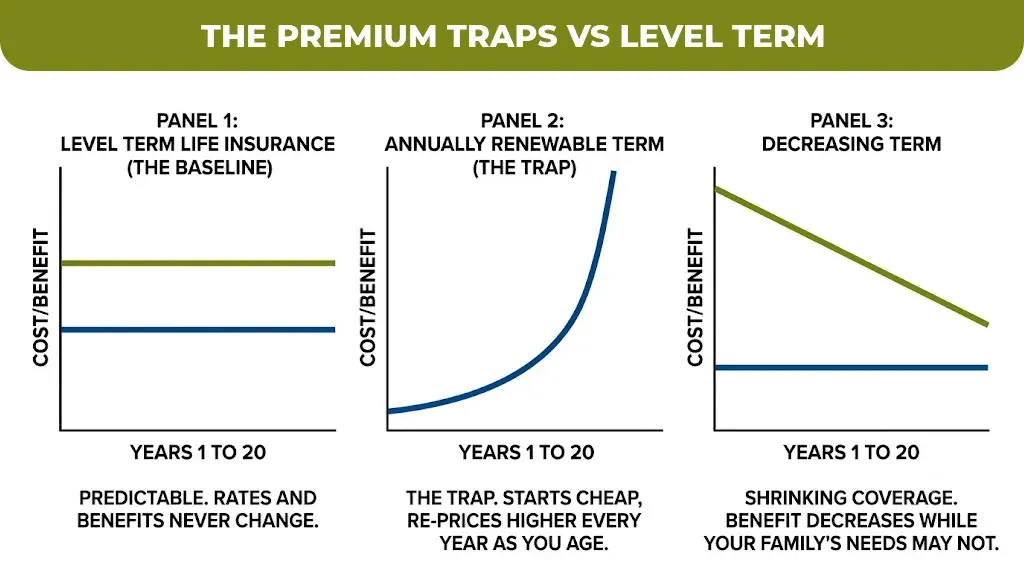

Annual renewable term life insurance policies are priced cheaply at first. The insurance company reprises your premium every year and it is based on your age. By the time you were dedicated into the policy the rate you are paying can be two or three times more than what you started with. You did not choose that. It was built in the structure from the beginning.

Term insurance policies were different. The premium will be paid on the first day at the same premium you are paying on the final day of the policy, regardless of how old you are or how your health has changed. That predictability is not the small benefit. Over a 20 or 30 year it can save a family tens of thousands of dollars as compared to the policies that reprise annually.

What Is Level Term Life Insurance?

The term life insurance policies are policy that fixes both your monthly premium and your family’s death benefit for the time that can be generally 10, 15, 20 or 30 years.

The word “level” refers to this consistency. Your rate does not increase with your age. Your death benefit does not decrease over time. The insurance company takes on the risk of locking that rate, and you gain the predictability of knowing exactly what you will have to pay and what your family will receive throughout the policy.

This is the difference from decreasing term life insurance, where the death benefit drinks overtime and from annually renewable terms where the premiums reprice every year.

For most families in 2026, level term is the recommended baseline. It is simple, transparent, and affordable.

How Does Level Term Life Insurance Work?

The level term life insurance work in very simple steps for that you have to choose a coverage amount, a term length and the premium. Your policy will stay active and your family will receive the death benefit if you pass away as long as you are paying your premiums on time.

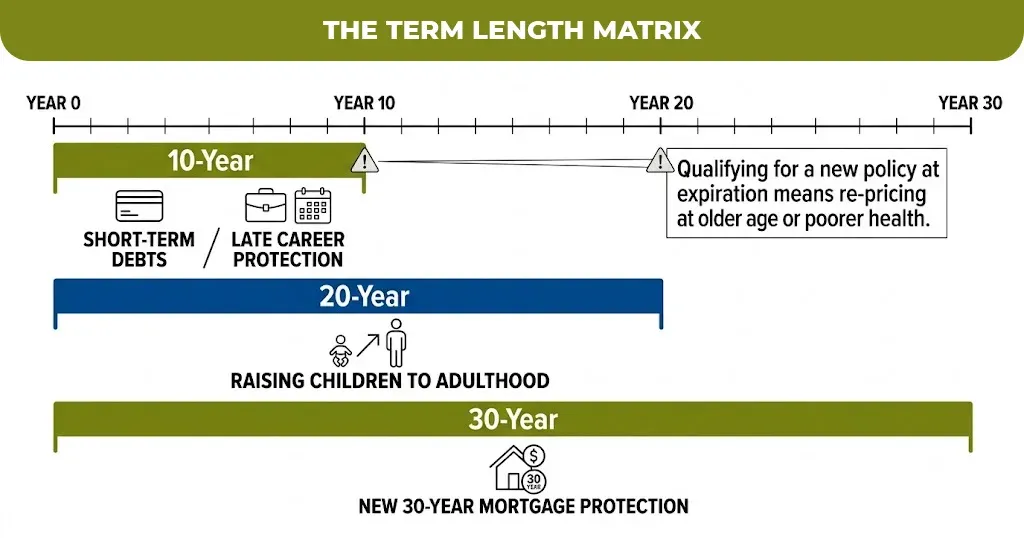

If you outlive the term, the policy expires. There is no payout, and coverage ends unless you renew or convert to a permanent policy. Renewal at that point is typically at a much higher rate because you are older.

That is why choosing the right term length upfront matters more. Buying a 10 year policy at 45 years and then needing to renew at 55 means qualifying for a much higher rate during the period when your health may have changed.

According to Forbes Advisor, 82 percent of Americans over 25 overestimate the cost of life insurance. The reality is that the level term coverage is often far more affordable than the most people expect, particularly for buyers in their 30s and 40s.

Level Term Life Insurance Rates in 2026: What You Actually Pay

The rate chart we are waiting come from 2026 market data and it reflects non-smoking applicants in good health. For your plan the rate can be different and it be based on your class your state and insurance company.

Average Monthly Rates for a $500,000 Level Term Policy (Non-Smoker, Good Health)

| Age | 10-Year Term | 20-Year Term | 30-Year Term |

| 30 (Male) | $19/mo | $38/mo | $62/mo |

| 30 (Female) | $16/mo | $31/mo | $50/mo |

| 40 (Male) | $41/mo | $59/mo | $104/mo |

| 40 (Female) | $34/mo | $47/mo | $82/mo |

| 50 (Male) | $93/mo | $137/mo | Not widely available |

| 50 (Female) | $74/mo | $110/mo | Not widely available |

Level Term vs. Decreasing Term: The Difference That Matters

These two policy types are frequently confused, and choosing the wrong one can leave your family significantly underprotected.

Level term life insurance keeps the death benefit constant throughout the policy. Your family receives the same payout whether you die in year one or year nineteen.

Decreasing term life insurance reduces the death benefit over time, usually in line with an outstanding debt like a mortgage. Premiums may be lower, but your coverage is shrinking while your family’s need for that coverage may not be.

The key question is what you are protecting. If your primary goal is income replacement for your family, level term is the right choice. If you are specifically covering a repayment vehicle like a home loan and want nothing else, decreasing term may reduce your premium. But for most families, level coverage offers better value and more flexibility.

What Affects Your Level Term Life Insurance Rate

Knowing what drives your premium helps you shop smarter and avoid overpaying.

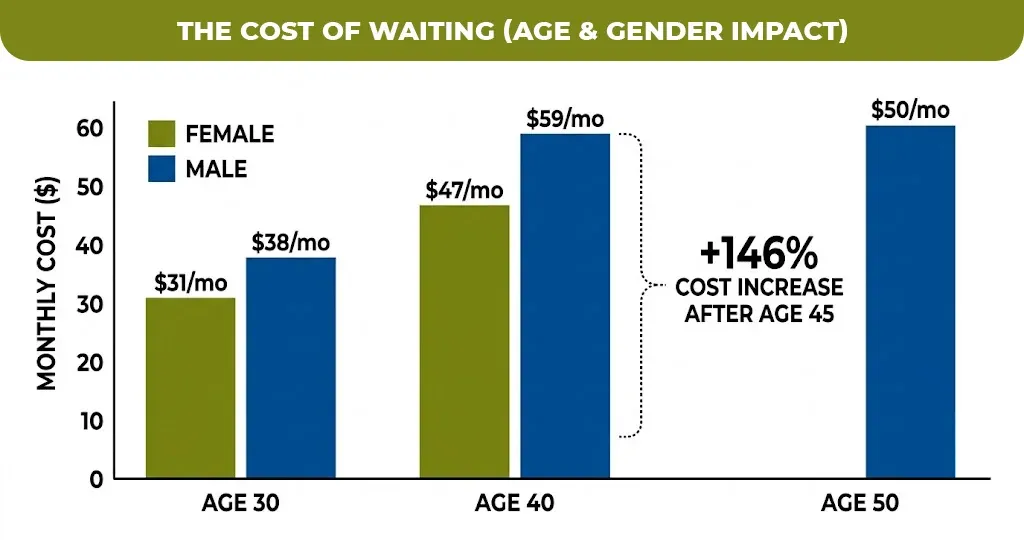

Age is the largest single factor. Rates rise gradually through your 30s and then sharply after 45. A 50-year-old male pays 146 percent more than a 40-year-old for the same coverage.

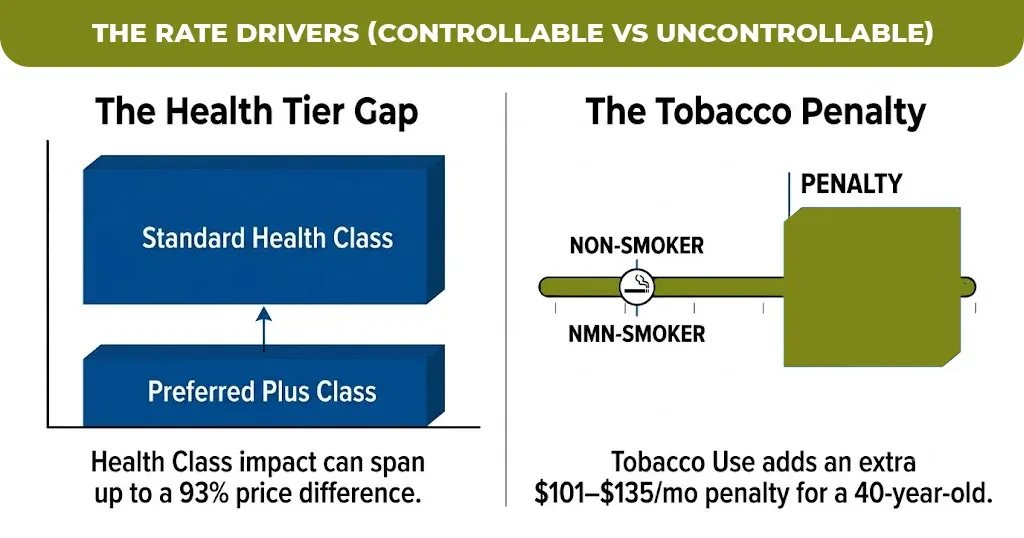

Health class creates a significant premium spread. The same policy at Preferred Plus versus Standard health class can differ by up to 93 percent in monthly cost, according to InsuranceGeek’s 2026 data.

Tobacco use is the largest controllable cost factor. A person who is 40 years old and he’s a smoker have to pay around $101 $135 or even more than that per month as compared to the person who is not smoking for the same $500,000 policy for 20 years term.

Gender affects rates because women statistically have longer life expectancy. A 40-year-old woman pays approximately $12 less per month than a man of the same age for identical coverage.

Coverage amount and term length both increase cost, but not proportionally. The cost per $1,000 of coverage decreases as coverage levels increase, meaning a $1,000,000 policy is not twice as expensive as a $500,000 policy.

Compare life insurance coverage options and what each one protects (internal link placeholder)

The Advantages and Disadvantages of Level Term Life Insurance

Advantages

Predictable cost throughout the full policy period. No annual rate increases. Simplicity: you pay, your family is protected. Affordable access to significant death benefit coverage. Flexibility to choose the term that matches your actual financial obligations.

Disadvantages

No cash value accumulates. If you are still alive after your term and then there is no return on the premiums that are paid. For that you have to renew the policy after expiration and you also require the qualifying at the current age and your health status of an a significantly more rates.

Finding the Right Level Term Policy Without Overpaying

The rate you are quoted from one carrier is not the best rate that is available to you. The insurance companies price the same policy differently and they spread between the carriers for identical coverage that can exceed 50%.

Work with an independent broker or use a multi-carrier comparison tool to see what the actual market looks like for your age, health, and coverage amount. Applying early, before a health change or birthday, is consistently the most effective way to lower your long-term cost.

If you want guidance on finding the right term length and coverage amount without pressure or upselling, the team at MLife Insurance can walk you through a comparison across multiple carriers based on your specific situation. There is no obligation and no script, just a clear answer to what you actually need and what it will cost.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.