Your agent quoted that you can get a plan $800 a month for the whole life. You think it sounds too expensive but you are afraid that a cheap policy might leave your family exposed. So you start searching for the alternatives and someone mentions that guarantee universal life insurance. Now you are comparing three products you don’t fully understand and you are also worried what if you will pick the wrong one

That confusion is exactly where costly mistakes happen.

Guaranteed universal life insurance is not for everyone, but for the right person especially someone who want permanent life coverage without paying for a cash value they will never use, it can be one of the most cost-effective decision in the financial planning. Here is what it is actually, what it cost in 2026 and who should buy it.

What Is Guaranteed Universal Life Insurance?

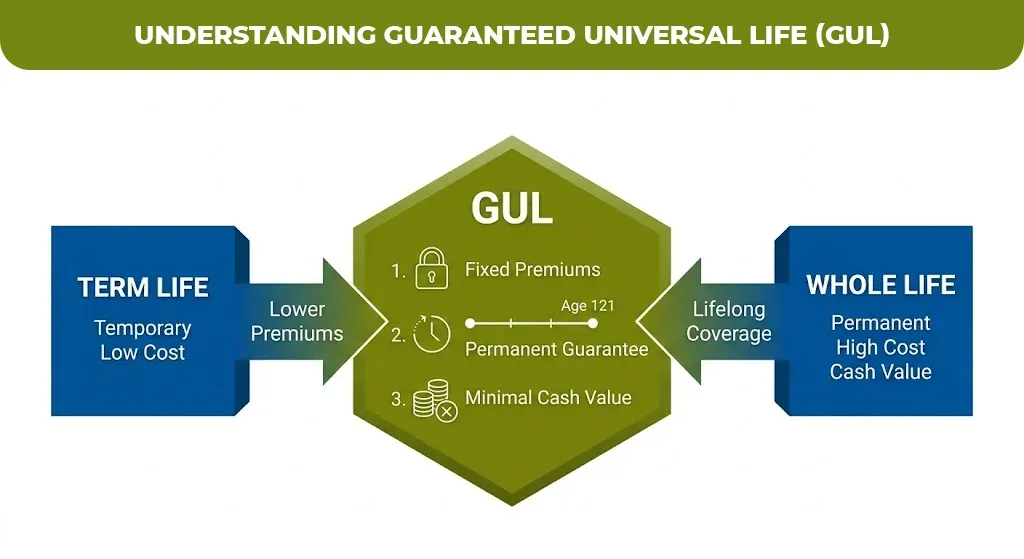

Guaranteed universal life insurance is a type of permanent life insurance plan that will give you are locked in debt benefit with fixed premiums, without building the significant cash value. Think of it as term life insurance that is extended to age 90, 100 or even 121.

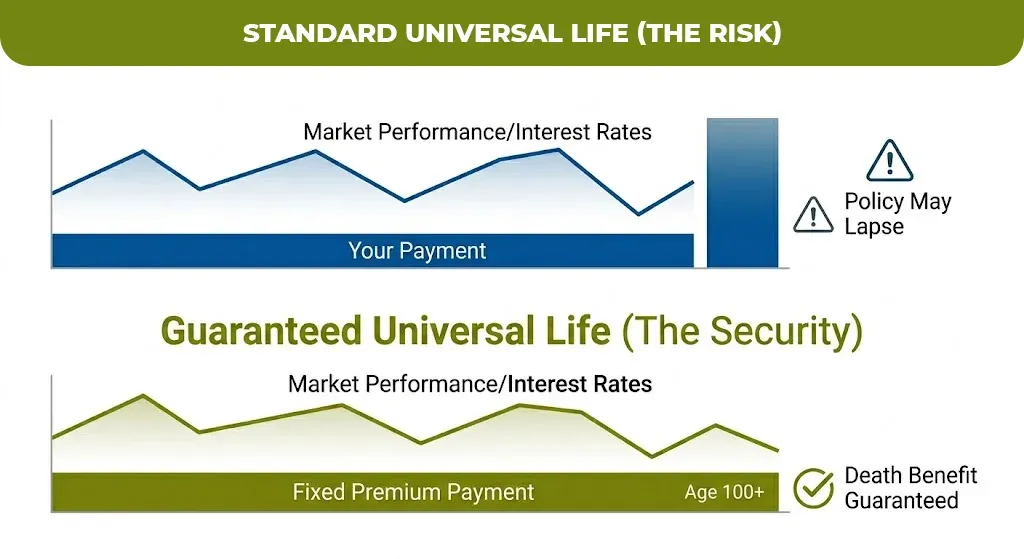

The standard universal life policies will depend on the interest earning or market performance to keep the policy funded. If those returns fall, your premiums will go up at the policy lapse. Currently universal life insurance will remove that uncertainty entirely. As long as you are paying the required premium then the insurance company will guarantee that that benefit that is stay enforced until the age you choose regardless of the interest rate or the market conditions.

According to Ethos Life, GUL is often described as a hybrid between term and whole life: it provides lifelong coverage like whole life, but without the investment component that drives whole life premiums up.

How Does Guaranteed Universal Life Insurance Work?

The mechanics are straightforward. You apply for a coverage amount for example, $250,000 or $500,000), select the age you want coverage guaranteed to typically 90, 95, 100, or 121, and pay a fixed premium that never changes. The insurer guarantees that as long as that premium is paid on time, the death benefit will be paid to your beneficiaries.

What makes GUL different from standard universal life is the no-lapse guarantee rider. This provision is the backbone of the policy. Without it, a traditional universal life policy can fail if the policy’s internal fund runs low, a scenario that has blindsided many seniors on fixed incomes who thought they had permanent coverage.

The trade-off is minimal cash value. Most GUL policies in 2026 build little to no cash value, meaning if you surrender the policy early, you’ll receive very little back. That’s intentional — the lower premium exists precisely because the insurer isn’t funding a savings component.

Guaranteed Universal Life Insurance Pros and Cons

Before you commit, here’s an honest assessment of what GUL does well and where it falls short:

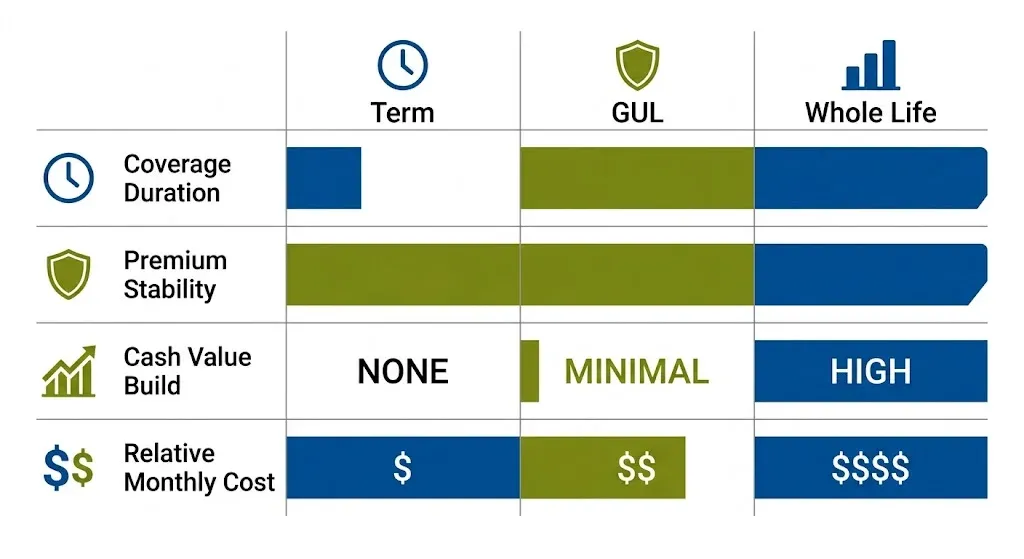

| Factor | GUL | Whole Life | Term Life |

| Death benefit guaranteed? | Yes | Yes | Yes (within term) |

| Premium stays fixed? | Yes | Yes | Yes (within term) |

| Builds cash value? | Little to none | Yes (significant) | No |

| Coverage end date | Age 90, 100, or 121 | Lifetime | 10, 20, or 30 years |

| Monthly cost (age 40, $500K) | $310 – $362 | $765 – $930 | $53 – $59 |

| Surrender value if cancelled? | Minimal | Moderate to high | None |

The Core Pros

GUL costs 30–50% less than a comparable whole life policy for the same death benefit, according to Insurance By Heroes. For someone whose goal is simply to leave money behind, not to build savings, this difference is substantial.

Premiums are completely immune to interest rate swings. Unlike traditional universal life, there is no scenario in which the insurer comes back and asks for more money because the market underperformed.

The Core Cons

If your financial goals shift and you need to access cash from your policy, GUL offers very little. There’s no meaningful loan value, no tax-advantaged savings you can tap in retirement. It is a one-purpose tool.

If you miss premium payments, the no-lapse guarantee can lapse. Some carriers require strict on-time payments to keep the guarantee active, which is a risk for anyone on a variable income.

Guaranteed Universal Life Insurance for Seniors: What Changes Over 70

For seniors, GUL is often the most practical form of permanent coverage available. Here’s why.

Term life becomes nearly impossible to qualify for past age 70, with most carriers capping new term policies at 75 or 80. Whole life premiums become prohibitively expensive. Guaranteed issue policies, the ones with no medical exam, cap out at $25,000 to $30,000 in coverage, which covers a funeral but not an estate.

GUL sits in the middle. Most GUL carriers accept applications up to age 80 or 85, and even with a medical exam, many seniors in average health qualify at reasonable rates. The policy then guarantees coverage to the selected end age, providing the certainty that term insurance cannot.

Is Guaranteed Universal Life Insurance Worth It? The Honest Answer

For the right buyer, yes it is worth it. For the wrong buyer, you will pay for certainty you did not need and miss out on financial tools you did.

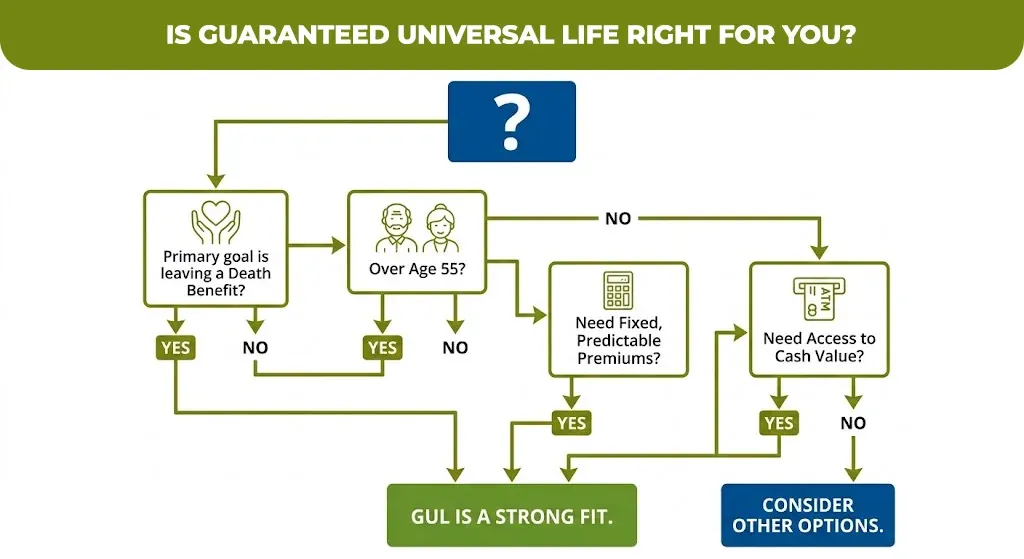

Gul Is Worth It When

- Your primary goal is to leave a death benefit, not to grow money inside a policy

- You are over 55 and term life no longer makes sense given your coverage timeline

- You are on a fixed or predictable income and need premium certainty above all else

- You are doing estate planning and need a guaranteed, tax-free transfer of wealth to heirs

Gul Is Not Worth It When

- You need access to cash value during your lifetime

- You are under 45 and term life would cover your dependent years at a fraction of the cost

- You want market participation or any form of investment growth inside your policy

The IRS will allow the death benefit from a GOL policy to pass the income tax free to your beneficiaries under IRC Section 101(a), which will make it a particularly efficient estate planning tool for the seniors who are concerned about the inheritance of Texas.

How to Buy Guaranteed Universal Life Insurance Without Overpaying

The biggest mistake buyers make is accepting the first quote from a single carrier. GUL pricing varies significantly between insurers, sometimes by 20–35% for the same coverage and age because each carrier runs its own actuarial models and risk tolerance.

Work with an independent broker, not a captive agent who represents one company. An independent broker can pull quotes from Pacific Life, Protective Life, Corebridge, Banner Life, and others simultaneously, letting you compare real numbers side by side.

Also confirm these three things before signing:

- The no-lapse guarantee is explicitly stated in the policy contract, not just in the illustration

- The carrier holds an AM Best rating of A or higher, confirming long-term financial stability

- The premium structure is defined for a specific coverage age (e.g., age 100), not open-ended

Thinking Through Your Options? Mlife Insurance Can Help

If you are reading this to figure out whether GUL is the right fit for your situation, that question is actually the right place to start. Many people buy a whole life because it sounds safe, term because it sounds cheap, and end up with neither fitting their actual needs five years later.

The team at mlife Insurance works through exactly these comparisons with clients regularly, helping you look at real carrier quotes, understand what the guarantee actually covers, and match the policy structure to your financial goals.

If that conversation sounds useful, it costs nothing to start one.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.