That is not an insult. It is a documented pattern. And New are among the most commonly misunderstood financial product in the retirement space and buying the wrong one or the misunderstanding what you own can cost you a lot of money in the cylinder charges, loss flexibility or the prices you never saw coming.

The annuity definition most people get is either too vague to be useful or buried in the insurance jargon again that will not help you to make a real decision. The article gives you the easy understanding, the types that matter and the number you need to understand before signing anything.

Definition Of Annuity: What It Actually Means In Plain Terms

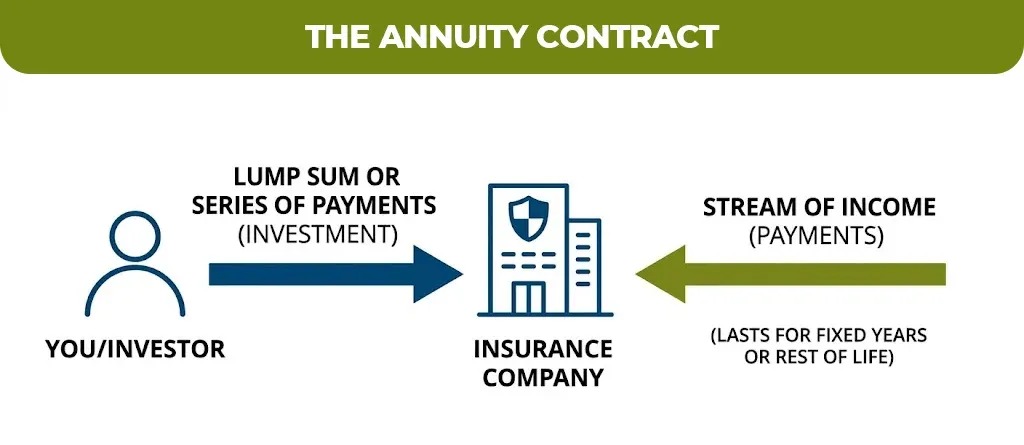

An annuity is the contract between you and an insurance company where you have to pay a lump sum of the series of payment, and in return the insurance company will pay you a stream of income either immediately or at the future date.

That’s the important annuity definition in finance. The income stream can last for a fixed number of years or for the rest of your life, depending on which type you choose and how the contract is structured.

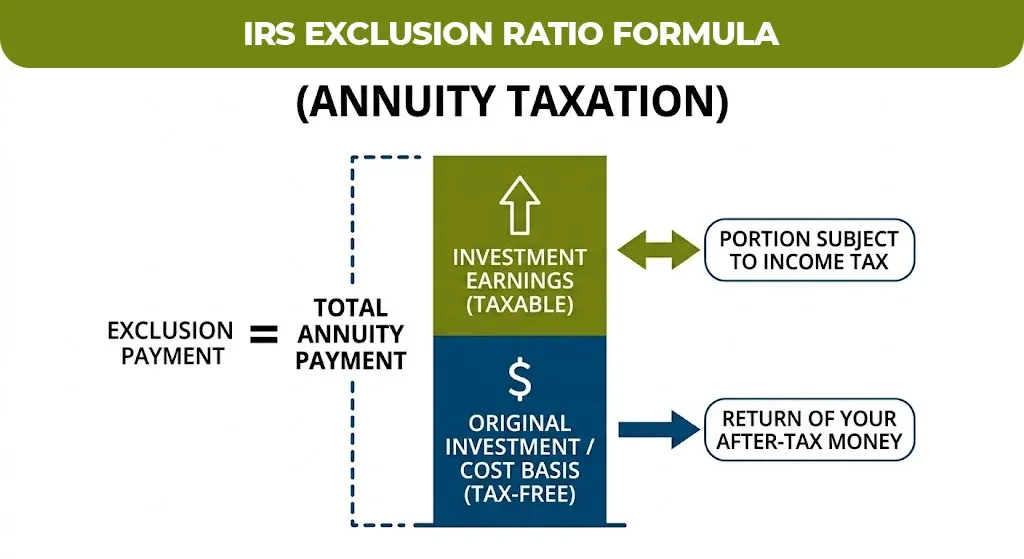

According to the IRS Publication 575, annuity payments may consist of both a return of your original investment (cost basis, which is tax-free) and investment earnings (which are taxable). Understanding that split is essential before you take your first payment.

The Types of Annuities You’ll Actually Encounter

This is where the most explanations fall apart. There are six primary types, and each one serves a different purpose. Using the wrong one for your situation is the real and expensive mistake.

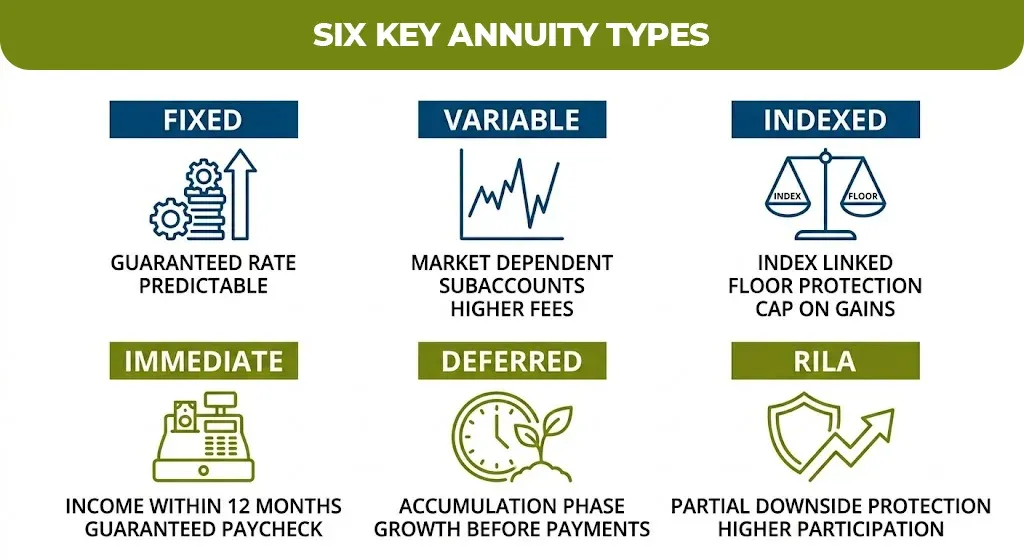

Fixed Annuity

The fixed annuity definition is the simplest: the insurance company guarantees a specific interest rate for a set period. Your money grows at that rate regardless of market conditions. This suits people who want predictability above all else.

Variable Annuity

The variable annuity definition involves investment subaccounts, similar to mutual funds. Your return depends on market performance. The upside is growth potential that the downside is that your income can go down if markets fall. According to FINRA’s guidance on variable annuities, fees in these products can be significantly higher than comparable mutual funds, which eats into returns over time.

Indexed Annuity / Fixed Index Annuity

The fixed index annuity definition sits between fixed and variable. Your growth is linked to a market index like the S&P 500, but with a floor that protects you from losses. The indexed annuity definition also includes caps that limit your upside, so you don’t capture full market gains either.

Immediate Annuity

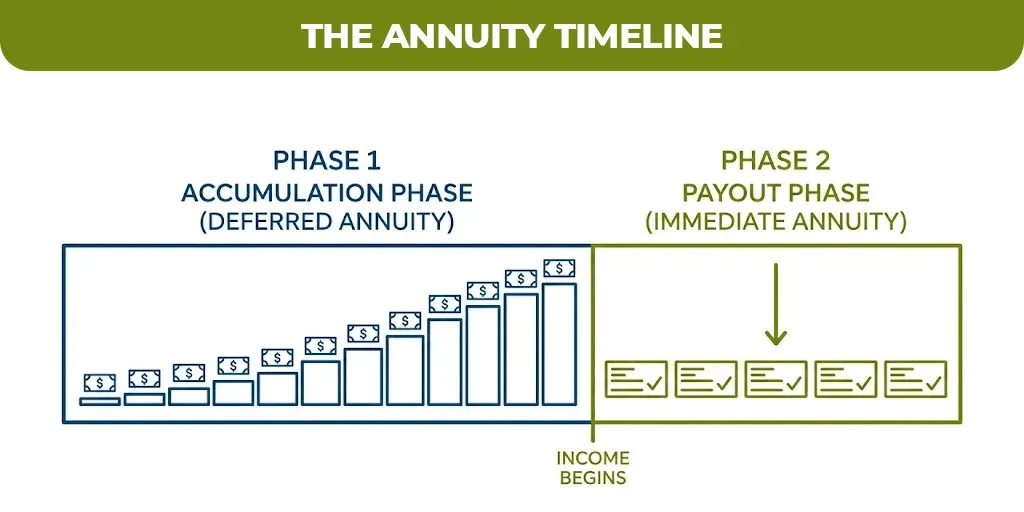

The immediate annuity definition is exactly what it sounds like that you pay a lump sum and income payments begin within 30 days to 12 months. This is the product most closely associated with the annuity income definition, because it converts savings directly into a guaranteed paycheck.

Deferred Annuity

The deferred annuity definition covers products where your money grows during an accumulation phase before income payments begin. Most annuities sold today are deferred products.

RILA (Registered Index-Linked Annuity)

The RILA annuity definition is newer. These products offer partial downside protection in exchange for a higher participation rate in market gains than traditional indexed annuities. RILA sales reached $20.7 billion recently, making them one of the fastest-growing categories in the annuity market.

Ordinary Annuity vs Annuity Due: A Distinction That Affects Real Money

The ordinary annuity definition refers the payment that is made at the end of the age period. The annuity due definition means that the payment comes at the beginning of each period.

This matters in the retirement in complaining because the timing of the payment affects the present value of the contract. An NUT due is worth slightly more than an ordinary annuity with the identical terms because you receive each payment one period earlier.

When you are evaluating the annuity payment definitions in the contract, always make sure to confirm if the payments are structured as an ordinary annuity or annuity due, as this changes you are actual income timing from one day.

Tax Treatment: What the IRS Says About Annuity Income

The annuity taxation depends on if the money inside the contract was contributed pre-tax or after tax.

If you find an annuity with the pre-tax money such as rolling over a traditional IRA, then all the payments are fully taxable as ordinary income when withdrawn. If you use after tax dollars, then only the earnings portion of each payment is taxable not the return of your original contribution.

The IRS exclusion ratio formula determines what percentage of each payment is tax free. For a tax-sheltered annuity (TSA), which is a 403(b) plan annuity available to school employees and nonprofit workers, contribution limits in 2026 follow standard IRS 403(b) caps. Contributions to these plans grow tax-deferred until withdrawn.

Annuity Market in 2026: Why These Products Are Growing

The annuity insurance definition has expanded in practice alongside the product market itself. The global annuity market was valued at $6.45 billion in 2025 and expanded to $6.85 billion in 2026, driven by rising retirement planning and income security needs.

Three forces are driving that growth. First, the longer expectancies means that retirees need income to last 25 to 30 years, not 10 to 15.

Second the shift from pension plans to self-directed 401K means individual now carry longevity risk that employers once handled.

Third, the median annual household income for the Americans who are 65 years and older is $56,680.

According to the census bureau data and for many households, the annuity income is what bridges the gap between the Social Security and actual living cost.

The charitable gift annuity definition is also worth noting for philanthropically minded retirees: you donate an asset to a nonprofit, which in return provides you with fixed annuity payments for life. This combines income planning with charitable giving in a single structure.

Understanding Annuities Before You Commit Protects More Than Your Money

The right annuity, that is bought at the right time for the right reason is one of the most reliable retirement income tool that is available. The wrong one, that bought without understanding the terms can lock you into a product that will cost far more than it pays back.

If you are working through the retirement in complaining and want to understand how any products fit into a broader life insurance and financial protection strategy then the team at Mlife insurance will help you and walk you through your options without any pressure.

Understanding what you’re buying matters more than buying quickly. Take the time to get it right.

Explore annuity and life insurance options with Mlife Insurance

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.