Key Points

- High premium costs

- Cash value growth

- Long-term commitment required

- Service quality varies

Most people searching for “ life insurance savings group” are standing at the crossroads when they have seen an ad, got a call, or been referred by a friend, and they are not sure if this is a genuine financial product or a clever marketing wrapper that is designed to separate them from their money.

Here is the truth, the life insurance savings group model is real, but it is not one-size-fits-all. Make the wrong call, and you will be paying premiums for a policy that under delivers on cash value for years.

This guide cuts through the noise. No jargon, no fluff, just the fact you need to decide.

What Is a Life Insurance Savings Group?

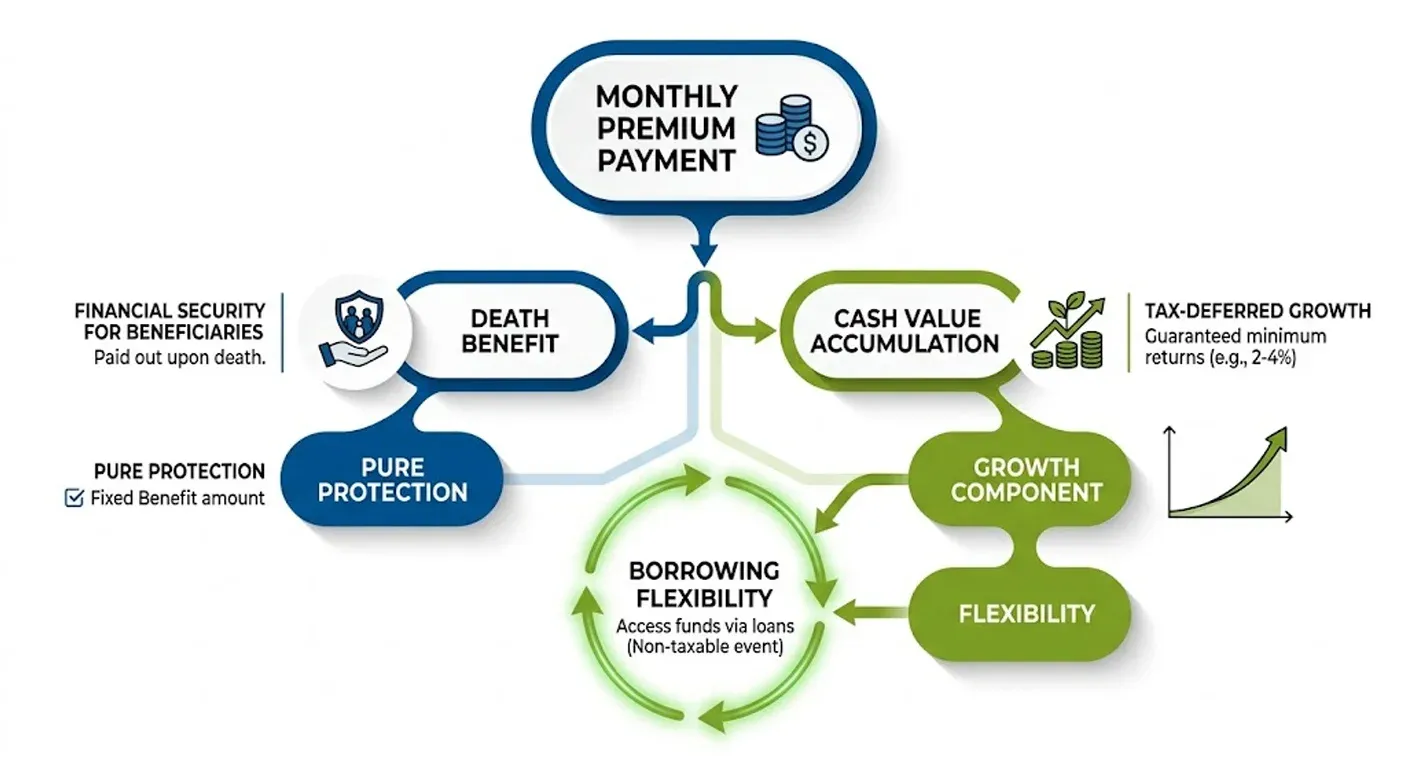

Life insurance savings group LISG is a financial services organization that bundles life insurance coverage with a cash value savings component, typically through whole life or index universal life insurance policies.

Is very straightforward, instead of a pure death benefit, your premiums also accumulate savings you can borrow against or withdraw later during your lifetime.

According to LIMRA’s 2025 Life Insurance Industry Report, roughly 54% of American adults now see permanent life insurance with a savings element as a viable alternative to traditional savings accounts amid rising inflation and rate volatility.

LISG operates primarily through direct sales channels like the agents who contact the potential clients via phone, referrals, or digital outreach. There are so many of these agents that are independent contractors working under third-party business process outsourcing arrangements, which means the customer support you reach after enrollment may not be in house staff.

How Life Insurance Savings Group Works

LISG sells permanent life insurance products that double as savings vehicles. Here are the basic mechanics.

You pay monthly premiums

You have to pay monthly premiums like a portion that covers the death benefit that funds a cash value account.

Cash value grows tax-deferred

The cash value grows tax deferred typically at a guaranteed minimum rate 2 to 4% or type to a market index with the cap.

You can borrow against the cash value

You can borrow against the cash value without triggering a taxable event, unlike a 401K withdrawal.

Payout on death

Your family gets payout on death, your beneficiaries receive the face value of the policy.

Life Insurance Savings Group Cost: What You’ll Actually Pay

LISG cost very significantly based on the age, health class, coverage amount and policy type. Here is the realistic 2026 snapshot.

Table 1: Estimated Monthly Premiums by Profile

| Profile | Coverage Amount | Policy Type | Est. Monthly Premium |

| 30-year-old, non-smoker, male | $250,000 | Whole Life | $180–$240 |

| 40-year-old, non-smoker, female | $250,000 | Whole Life | $260–$340 |

| 45-year-old, smoker, male | $250,000 | IUL | $420–$560 |

| 35-year-old, non-smoker, female | $500,000 | IUL | $310–$400 |

These premiums are 2 to 4 times higher than term life insurance for the same benefit but they include the same component. If you only need a death benefit, the term is cheaper. If you want the same later, permanent life insurance makes sense.

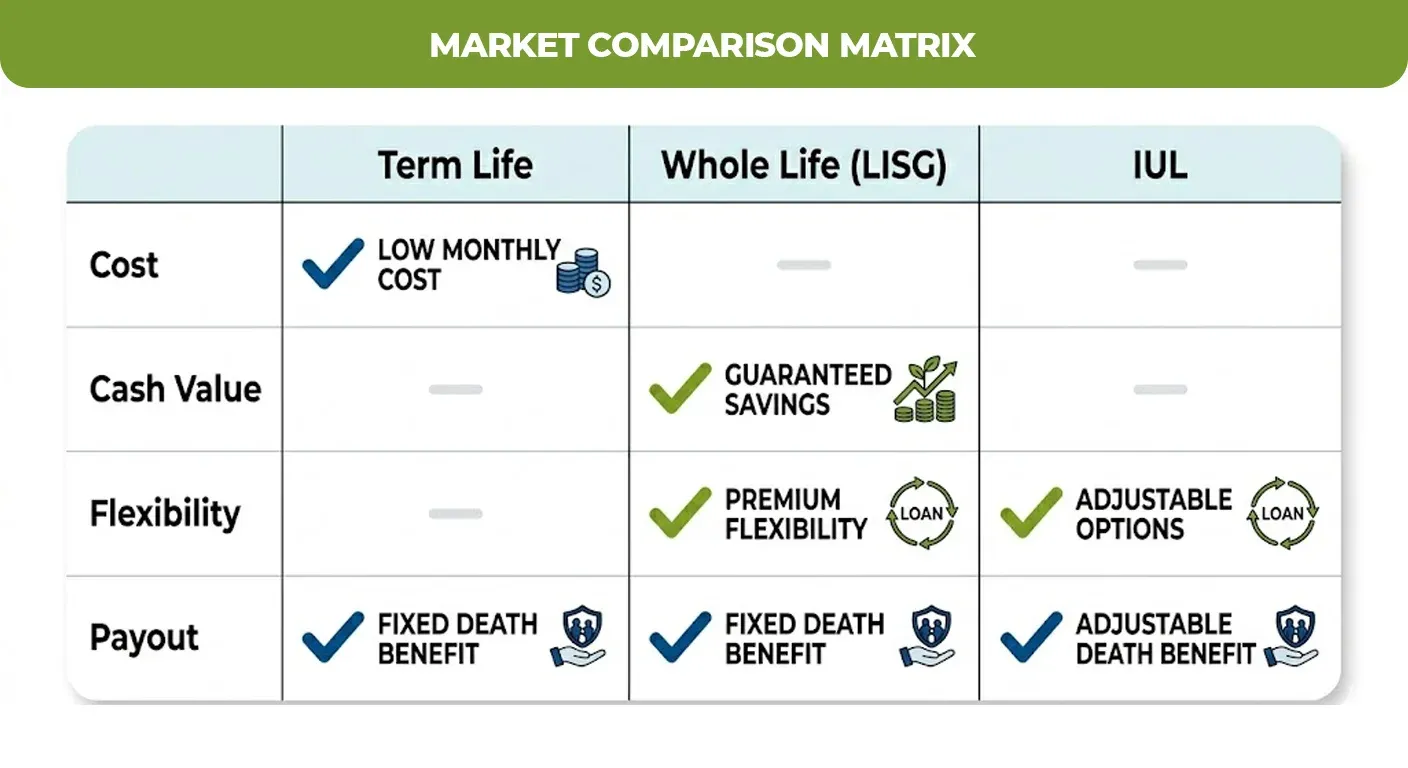

Table 2: LISG vs. Term vs. IUL — Quick Comparison

| Feature | Term Life | Life Insurance Saving Group (Whole Life) | IUL |

| Monthly cost (35, $250K) | $25–$35 | $200–$280 | ~$150–$220 |

| Cash value buildup | None | Yes, guaranteed rate | Yes, market-linked |

| Flexible premiums | No | No | Yes |

| Death benefit | Fixed | Fixed | Adjustable |

| Best for | Pure income replacement | Guaranteed savings + coverage | Growth-focused savers |

Life Insurance Savings Group Reviews: What Real Customers Say

Reviews of life insurance savings groups are split as strong on products, inconsistent on service. Based on aggregated feedback from platforms including the Better Business Bureau, trust Violet and Google reviews as of Q1 2026.

Positive patterns

- Customers who stay with their policies 8 to 10+ years report solid cash value accumulation

- Agent praised for a clear explanation at point of sale

- Multiple policyholders have no tax advantages as a key benefit.

Negative patterns

- Post sales customer support is frequently cited as slow or unresponsive

- There are several reviewers who noted confusion about the policy terms they had not been clearly explained

- Cancellation process is described as cumbersome.

The service inconsistency is largely tied to how LISE distributes it itself and support work. When outsourced BPO partners handle different stages of a customer journey like sales, on boarding, servicing and the experience can field is joined. This is a structured issue directed to the consumer insurance space broadly, not unique to LISG.

Pros and Cons of Life Insurance Savings Group

Pros

- Dual purpose product

- Tax deferred growth

- Borrowing flexibility

- Permanent coverage

- Guaranteed minimum returns

Cons

- High premiums

- Slow early growth

- Surrender charges

- BPO servicing gaps

- Complexity

Is Life Insurance Savings Group Legit?

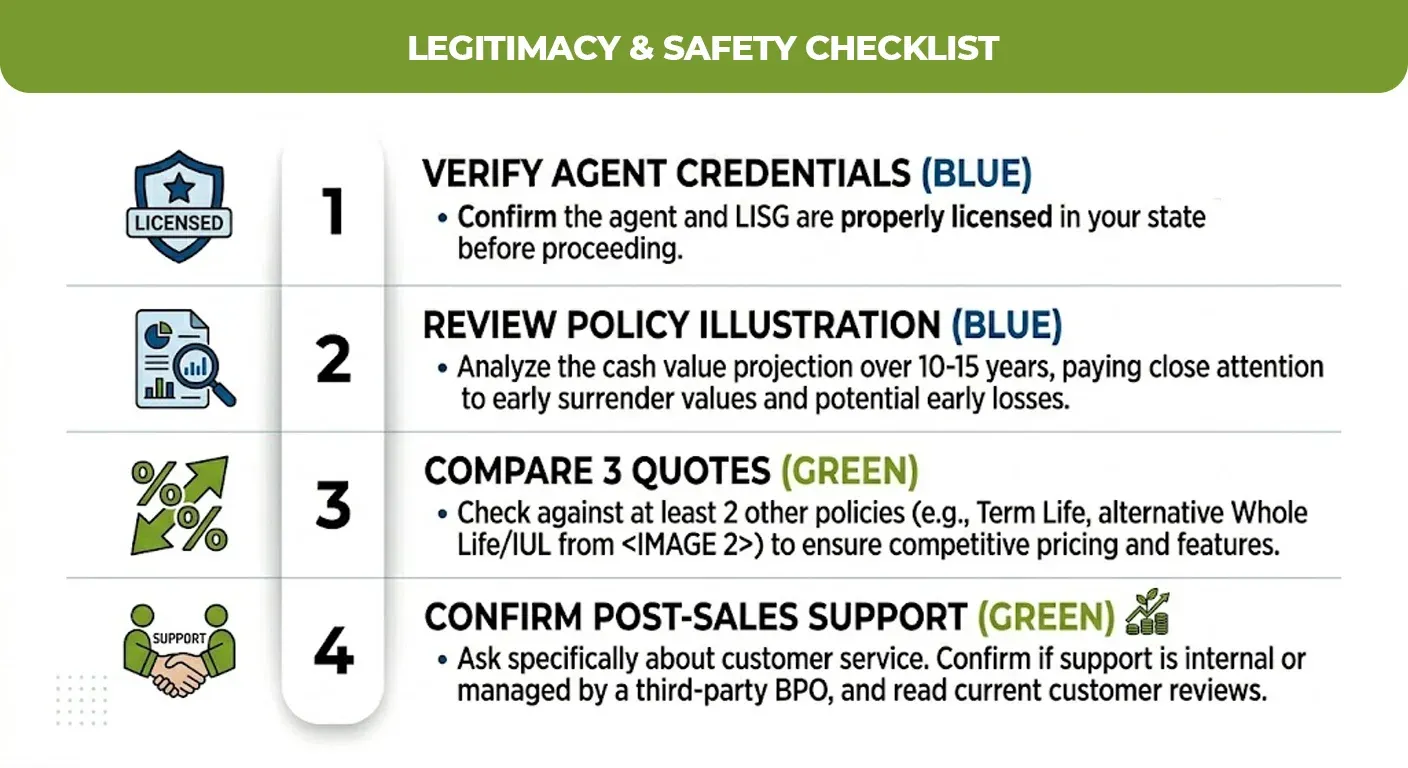

Yes, life insurance savings groups are legitimate financial services operations and not a scam or pyramid scheme. Its products are insurance policies underwritten by licensed carriers and subject to state insurance department oversight.

That’s it, legit does not automatically mean right for you. Here is how to protect yourself. Verify your agents license, read the policy illustration very carefully, ask who handles post sales support and make sure to compare at least 2 to 3 quotes from independent brokers.

Should You Choose a Life Insurance Savings Group?

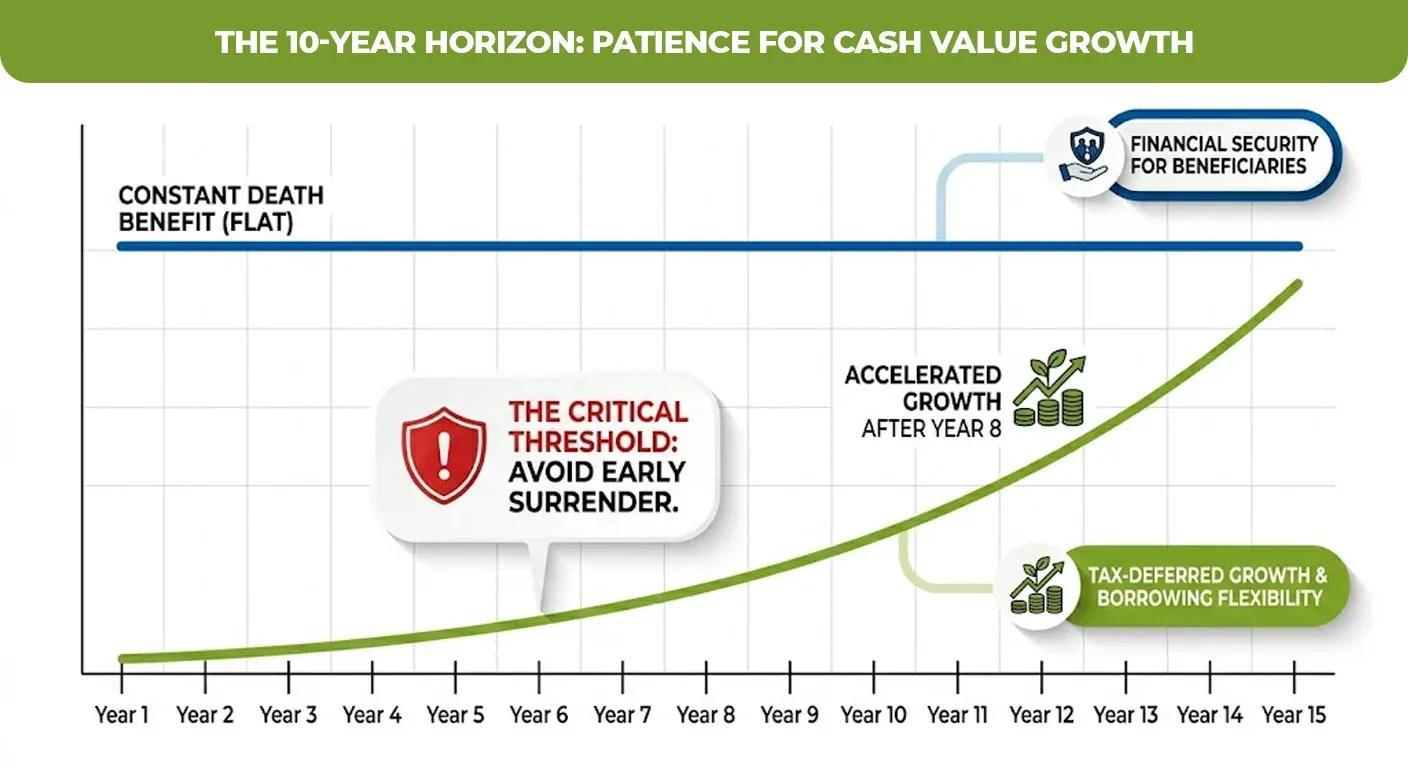

LISG is a good fit if you want permanent coverage, can afford the premiums and plan to hold the policy for at least 10 years. It is not the right choice if you are primarily looking for the affordable death benefit protection if you expect to need premium flexibility.

The savings component is genuine but it takes time to pay off. The biggest mistake people make is canceling in year 4 or 5 when cash value is still low, logging in a net loss.

Ready to Make the Right Call?

Navigating life insurance does not have to feel like a guessing game. At M-life Insurance, we are here to help people like you cut through the fine print and find countries that actually fits their life, not just their agents quota.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.