You assume that heart attack means life insurance is off the table and that assumption alone can cost your family real financial protection at exactly the moment they needed it most. The fear is understandable, but it is based on the outdated picture of how underwriting actually works today.

Can you get life insurance after a heart attack? Yes in nearly every case, though you will generally need to wait six months or two years after the event and expect a higher premium than someone without a cardiac history. Millions of Americans with a heart attack in their medical history carry the active life insurance policies right now.

Can You Actually Get Life Insurance After a Heart Attack?

Yes a heart attack does not disqualify you from life insurance but it does not trigger a wedding. And a more detailed underwriting review as compared to a standard application. Most insurance companies want to see at least six months to one year of stability before they will even consider your application and some required up to two years for more severe events.

The waiting period exist for the specific and practical reason. The American Heart Association notes that the risk of a second cardiac event is highest in the months immediately following the first one, which is exactly the window insurance company want to see you safely past before pricing your risk.

How Long Do You Actually Have to Wait Before Applying?

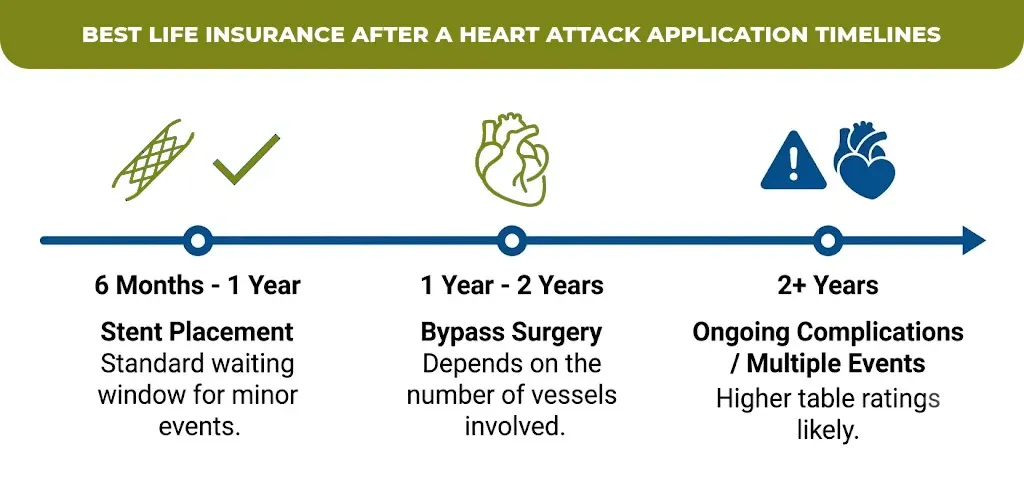

How long you wait depends on the severity of your heart attack and what treatment you received, ranging from about six months for a minor event with a stent to two years for more serious cases involving bypass surgery or ongoing complications. Applying too early is one of the most common and costly mistakes people make, since it often results in either an automatic postponement or an unnecessarily high rating that could have been avoided by waiting a little longer.

| Event Type | Typical Waiting Period Before Applying |

| Heart attack with stent placement | 6 months to 1 year |

| Heart attack with bypass surgery | 1 to 2 years, depending on vessels involved |

| Heart attack with ongoing complications | Up to 2 years |

| Multiple cardiac events | Often 2+ years, higher rating likely |

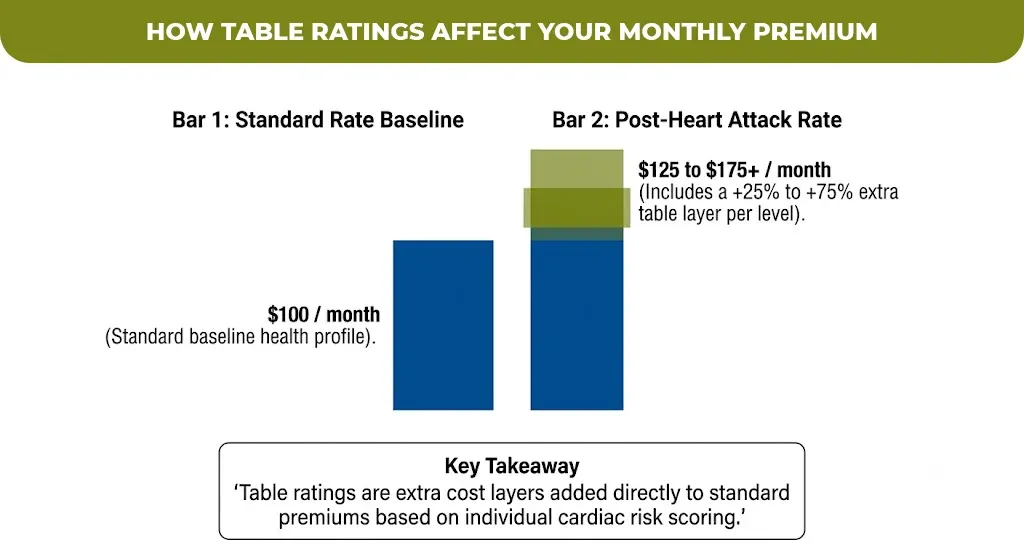

What Will Your Life Insurance Rate Actually Look Like?

Your rate after a heart attack typically comes with a table rating, an extra cost layered onto the standard premium, usually adding 25 to 75 percent per table level depending on the insurer. A standard policy that costs $100 per month might run $125 to $175 for a mild table rating, or considerably more for a higher one, depending on how your overall case is scored.

What Do Underwriters Actually Look At?

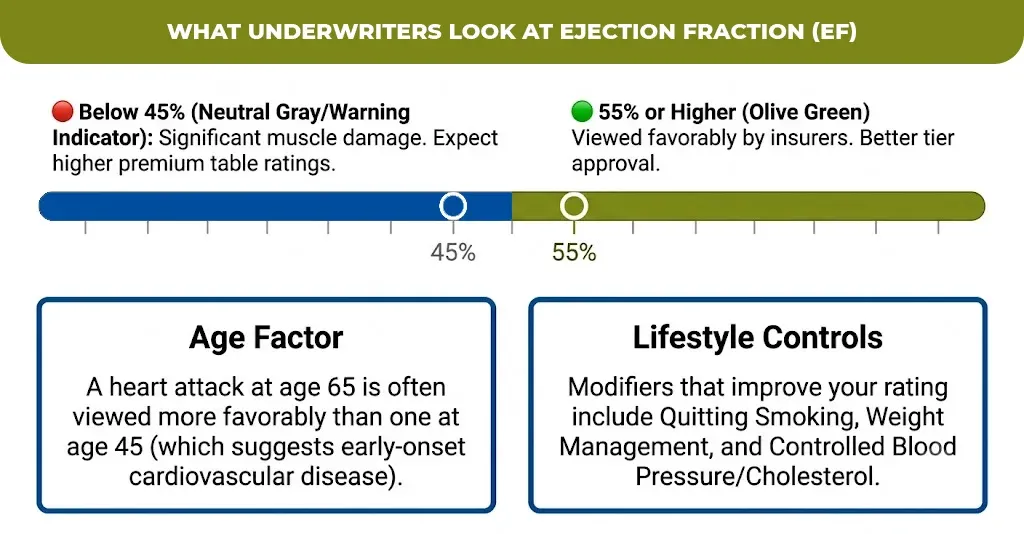

The underwriters focus more on your ejection fraction and the percentage of blood your heart comes out with each contraction, along with how much time has passed and how consistently you have followed your treatment plan. An ejection fraction of 55% or higher is generally viewed favorably. While a result below 45% generally signal is more significant heart muscle damage and pushes rate higher.

Your age at the time of heart attack also matters more than people expect. A heart attack at age 45 is generally viewed as more concerning than one at 65 since it can suggest earlier onset cardiovascular disease rather than an isolated age related event.

Beyond the cardiac-specific numbers, underwriters look at your complete health picture, not your heart in isolation. Quitting smoking, managing weight, and keeping blood pressure and cholesterol under control all factor into your overall risk profile and can meaningfully improve your rating even if your cardiac numbers stay the same.

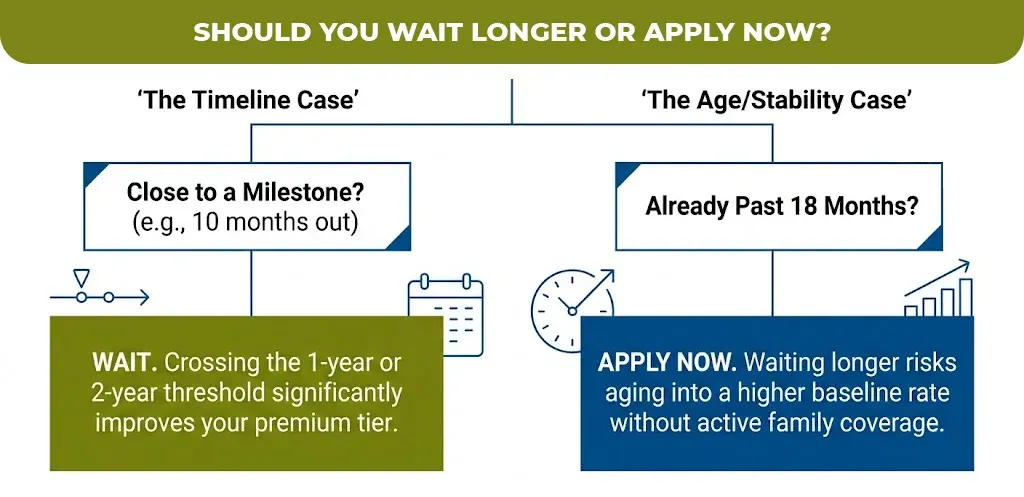

Should You Wait Longer or Apply Now?

Whether to wait depends on how close you are to a meaningful milestone, generally the one-year or two-year mark, balanced against the fact that your family has no coverage while you wait and that age itself will keep raising your premium regardless. If you’re 10 months out from your heart attack, waiting two more months to cross the one-year threshold can meaningfully improve your rating. If you’re already at 18 months with good stability, applying now often makes more sense than waiting another full year and aging into a higher baseline rate in the meantime.

There’s no single right answer here, since it depends on your specific timeline and how stable your recovery has been. Getting an actual quote now, even if you ultimately decide to wait, at least tells you where you currently stand instead of guessing.

What If You Can’t Qualify for a Traditional Policy Yet?

If you can’t qualify for traditional, fully underwritten coverage right now, simplified issue and guaranteed issue policies remain available as a bridge, typically without a medical exam but at a higher cost per dollar of coverage. Guaranteed issue policies usually include a graded death benefit period of two to three years, meaning if you pass away from natural causes during that window, beneficiaries receive premiums paid back rather than the full death benefit, though accidental death is typically covered immediately regardless of policy type.

This is a real tradeoff worth understanding clearly before choosing it. A guaranteed issue policy provides something rather than nothing while you build toward better underwriting eligibility, but it shouldn’t be mistaken for equivalent protection to a fully underwritten policy at standard or lightly rated terms.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.