Key Takeaways

- Cost effective loan coverage

- Declining payout structure

- Budget friendly premium

- Perfect for homeowners

- Matches debt balance

There are so many people who are looking for affordable life insurance that can fit a specific financial need, decreasing term life insurance becomes one of the most practical and cost-effective choices for them. The plan is especially popular among homeowners who want decreasing term life insurance for mortgage protection, also for the people who are paying off loans or anyone who needs coverage that will reduce their financial obligations.

In this detailed article we will explain to you about the decreasing term life insurance, it’s basic, how this plan will work for you and its different types. Also, we will decide what is the difference between level term or decreasing life insurance so let’s get started.

What Is Decreasing Term Life Insurance – A Basic Understanding

Decreasing term life insurance is a type of life insurance policy where the coverage amount reduces every year but your monthly premiums will stay the same. It means that the payout goes down over time, the cost remains unchanged, your policy becomes cheaper than the level term insurance and the coverage is aligned with the shrinking debts.

Because of its structure, design and simplicity this plan is widely used to protect the financial responsibilities that decline yearly like the mortgages.

In simple terms, this is a life insurance policy that is especially designed to match the debts that decrease over time.

Why People Choose Decreasing Term Insurance

People often choose to decrease term life insurance because this plan is used to cover the home costs, personal loan, business loan, car loans and any structured repayment plan.

The logic behind this is very simple as your loan gets smaller. Your insurance coverage also gets smaller. Because the payout reduces every year the insurance company charges less making this policy one of the cheapest life insurance options available.

Decreasing Term Life Insurance For Mortgage Protection

One of the most common uses of this plan is not case decreasing term insurance. Cases start high and then slowly reduce with the monthly payments. A decreasing policy follows this same pattern.

Here is how it will help the homeowners. If you pass away during the mortgage case term then the insurance payout covers the remaining loan, your family does not lose the home, no one can face the certain financial stress and your mortgage gets paid off automatically. This makes a decreasing term life insurance policy a perfect Mass for fixed rate mortgage where the loan decreases in a predictable way.

Choosing Level Term Or Decreasing Life Insurance – The Best Option Explained

There are so many people who become confused when deciding between the two. Here is the simplest way to choose

Choose Level Term Life Insurance If

- You want the same payout throughout the policy

- You want income protection for you family

- You want to leave a financial gift

- Your needs do not decrease over time

Choose Decreasing Term Life Insurance If

- Your main goal is to protect a loan or mortgage

- You want the cheapest possible coverage

- You only need insurance for the specific obligations

- You debt reduces every year

In simple words, level terms are best for family protection and decreasing terms are best for debt based protection.

Types Of Decreasing Term Insurance

Although the concept is very simple, there are so many different types of decreasing term life insurance policies. Choosing the right one will make sure that you get the proper financial coverage

Mortgage Based Decreasing Term Insurance

This is the most popular choice. In this plan the coverage decreases at the same pace as your mortgage balance.

Annual Reduction Policy

In this plan the coverage reduces by the fixed percentage each year like 5% or 10%.

Custom Reduction Schedule

In this plan you decide how fast the coverage decreases. This is best for business loans or irregular repayment plans.

Joint Decreasing Term Life Insurance

This plan is designed for couples sharing a mortgage. The policy pays out once usually on the first death covering the remaining mortgage.

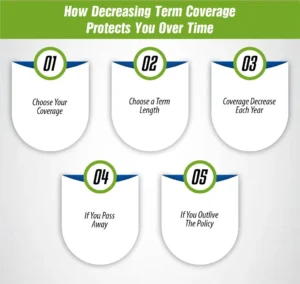

How Decreasing Term Coverage Protects You Over Time

Here is a very simple example to understand the decreasing term life insurance meaning

How Much Does Life Isurance Cost?

Choose Your Coverage

The first step is to choose your coverage. Most people choose their mortgage amount for example $200,000.

Choose a Term Length

Then the second step is to choose the term length that is 10,20,30 years.

Coverage Decrease Each Year

Your coverage decreases but your premiums stay fixed.

If You Pass Away

Your family will receive whatever coverage is left at that time.

If You Outlive The Policy

The plan ends with no payout like most of the term insurance plans.

How To Use A Decreasing Term Life Insurance Calculator

There are so many insurance companies that are offering the decreasing term life insurance calculator that shows

- Estimated monthly premiums

- How fast will your coverage be reduced

- Total cost of the policy

- Comparison with level term insurance

To calculate your quote, you will usually need the mortgage amount, policy terms, age, health status, your smoking habits and loan interest rate.

Benefits Of Decreasing Term Insurance

There are some the practical advantages of choosing a decreasing term insurance policy

Lower Monthly Premiums

Because the payout drops every year, the policy is cheaper than level term insurance

Designed for Mortgage and Loan

The plan is specially designed to protect the exact financial obligation you are paying off

Easy to Understand

There are no confusing features on investment components in this plan.

Fixed Premiums

The best thing is, your payments never increase even though the coverage decreases

You Pay Only What You Need

You avoid paying for unnecessary coverage and this is best for the budget friendly protection

How To Get Decreasing Term Insurance Quote

When you are requesting a decreasing term life insurance quote , you have to be prepared to answer your mortgage details, your desired coverage amount, loan type, health and your lifestyle information and if you want single or joint coverage. Comparing the multiple quotes from the different insurance companies will help you to find the best rate and the cover structure.

Is Decreasing Term Insurance The Right Option?

You should consider buying the decreasing term insurance policy if you have a mortgage

or a loan decreasing yearly, or you want low-cost life insurance. You can also buy this if you don’t need full level coverage, if you want predictable or fixed premiums. It can also be the best choice if you want financial protection only for the specific debt.

Final Thoughts

Decreasing term life insurance is very simple, budget friendly and a highly effective policy. This is best and designed especially for the home owners. Instead of paying for the coverage you don’t need, the policy reduces as your debt reduces, and makes sure that your family is protected at every stage.

Before choosing any plan you have to compare the different types of decreasing term insurance, review your mortgage schedule and decide whether level term or decreasing life insurance is best for your decision. With the right policy in place you can protect your family, secure your home and gain peace of mind knowing that your financial responsibilities will be taken care of.

Lets protect your home with M-life Insurance today! Get affordable, reliable mortgage protection that is specially designed to match your loan. You can also compare the plans, choose the right coverage and secure your families future with us.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.