Quick Facts About Short Term Disability Insurance

- Short-term disability insurance replaces the part of your income during illness or injury

- coverage lasts for 3 to 6 months depending on the policy

- The plan can cover pregnancy and maternity leave short-term disability insurance benefits

- Policies can offer by employer or purchase privately

- Benefits typically covered 50% to 70% of your income

- The waiting period is usually 7 to 14 days

- Cost depends on income, occupation and coverage amount

Life is so unpredictable. One day you are working as usual and the next day ,an illness, injury or pregnancy could keep you away from your job for weeks or months. Missing paycheck during this time can be very stressful and make it very hard to cover the everyday bills. That is where short -term disability insurance comes in.

In simple terms, short disability insurance provides temporary financial support while you recover and return to work. This coverage usually lasts for a few weeks to several months depending on the policy.

In this guide we will explain everything you need to know about short-term disability life insurance, via people choosing individual short term disability insurance if their employer does not offer it.

What Is Short Term Disability Insurance and Why It Matters

Short-term disability life insurance is a policy that is specially designed to replace the part of your paycheck if you cannot work for a temporary time because of a medical condition. This coverage usually begins after a short waiting period that is called elimination period. Once the waiting period ends then the insurance company starts paying a percentage for your regular income.

Here are some of the common situations that are covered by short-term disability insurance. These include

- Injury from accidents

- Surgery recovery

- Serious illness

- Pregnancy recovery

- Mental health conditions

- Temporary medical conditions

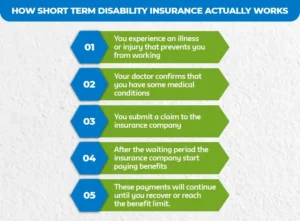

How Short Term Disability Insurance Actually Works

When you buy short-term disability insurance, then you choose a monthly benefit amount and coverage period. If you become unable to work due to any medical condition then you can file a claim with the insurance company.

This process usually works like

- You experience an illness or injury that prevents you from working

- Your doctor confirms that you have some medical conditions

- You submit a claim to the insurance company

- After the waiting period the insurance company start paying benefits

- These payments will continue until you recover or reach the benefit limit.

Most of the policies replace 50 to 70% of your salary which will help you manage the important expenses during the recovery.

Short Term Disability Insurance for Pregnancy and Medical Recovery

There are so many people who are interested in short-term disability insurance as pregnancy coverage. Pregnancy and childbirth can prevent someone from working for several weeks which is why disability coverage can also help to replace income during recovery.

With short-term disability maternity leave insurance, pregnancy can be treated as a temporary medical condition. The policy can provide benefits for pregnancy complications, recovery after childhood, doctor recommended bed rest and postpartum recovery. Coverage period can include six weeks for normal delivery and eight weeks for cesarean delivery.

However it is very important to note that the pregnancy is usually covered if the policy was purchased before becoming pregnant. Insurance companies considered pregnancy a pre-existing condition if it coverage starts after pregnancy begin begins

Maternity Leave Short Term Disability Insurance Explained

There are so many employers who offer maternity leave short-term disability insurance as a part of their benefits packages. This coverage will help replace the income during maternity leave when the parent is recovering after childbirth. This type of insurance does not usually cover the entire maternity leave period but focuses on the medical recovery time after delivery. There are so many companies offering short-term disability maternity leave insurance along with parental leave programs. In those cases the disability benefits will cover the medical recovery. While the parental leave covers the additional bonding time.

Employees should review their workplace benefits to understand how maternity leave and disability insurance work together for them.

Short Term Disability Insurance Not Through Employer: Private Options

There are some workers who do not receive disability coverage from their job jobs. In that cases, they can need short-term disability insurance not through employer programs.

All these policies are purchased directly from the insurance company and these are known as individual short-term disability insurance or short-term disability insurance.

Buying your own policy can offer you so many benefits like coverage stays with you if you change the job, it provides flexible benefit amounts, custom waiting periods and also coverage that is based on personal needs.

How to Choose the Best Short Term Disability Insurance Plan

Choosing the best short term disability insurance depends on your financial needs and job situation. Different policies have different benefits, waiting periods and coverage lengths. Whenever you are comparing the policies, you have to consider these important factors

- Choose a benefit that will cover your important expenses

- Make sure to look for the waiting period

- Look for the coverage options

- It’s important to confirm that the policy include regency benefits

- Make sure to look for the insurance company reputation

Short Term Disability Insurance Cost: What You Should Expect

The short-term disability insurance cost depends on the separate factors. Premiums are usually affordable as compared to long-term disability policies. There are some factors that affect the prices and these factors include your age, income, occupation risk, health history, benefit amount and waiting period time.

Aflac similarly states that you should expect to pay between 1% and 3% of your income for short-term disability insurance.

Top Short Term Disability Insurance Companies to Consider

There are so many well-known short-term disability insurance companies offering policies for individuals and businesses. These insurance companies provide flexible plans that can protect income during the temporary disabilities.

Whenever selecting a company look for the strong financial ratings, clear claim process, flexible coverage options and good customer reviews. Comparing the several providers will help you to find the right balance between cost and coverage.

Who Should Get Short Term Disability Insurance?

There are so many people who benefit from having short-term disability insurance. Coverage is especially helpful for workers who depend heavily on their income.

A study by LIMRA and Life Happens showed that over 60% of Americans would not be able to maintain their lifestyle after six months following a sudden illness or short-term disability. The effects of 6 months of income loss can be devastating, causing you to dip into your savings and setting you back in terms of retirement.

Final Thoughts: Is Short Term Disability Insurance Worth It?

Unexpected illness, an injury or pregnancy recovery can make it very difficult to work for several weeks or months. Without income protection, this situation can create serious financial challenges.

Short-term disability life insurance provides temporary income replacement so you can focus on recovery instead of worrying about the bills and expenses. Before choosing a policy, compare the coverage options, waiting periods and cost from different short term disability insurance companies. The right plan can provide peace of mind and financial support when needed most.

Protect Your Income with MLife Insurance

At M-life Insurance, we are here to help you compare the flexible coverage options that fit your needs and budget. Get expert guidance, compare the plans from trusted providers and find the right protection for your income

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.