7 Essential Facts About Disability Coverage

- This will replace your income if you cannot work

- Short-term disability plan covers temporary conditions

- Long-term disability plan protect against serious, long-term illness or injury

- Disability coverage benefits usually replace 50% to 70% of income

- Disability coverage plan cost depends on age, job and coverage amount

- Private disability insurance offers flexible and customized options

- Comparing the disability coverage quotes will help you to find affordable coverage

Life is so unpredictable. An accident or any illness can stop you from working for weeks, months and even for the years. Without income, it will become very difficult to pay the rent, mortgage , bills or any daily expenses. That is why disability coverage is very important. It protects your income and you cannot work due to any medical condition

In this detailed guide, you will learn what disability coverage is, how it works, the types of disability coverage , what are the coverage options and also how to get the right policy for your needs

What Is Disability Insurance and Why It Matters

This is the type of insurance that will replace a portion of your income if you become unable to work due to any illness or injury. There are so many people who think that health insurance is enough for them. But health insurance only pays your medical bills, but the disability income insurance can pay you money to cover the daily expenses

- It can cover rents or mortgage

- Utility bills

- Groceries

- Any loan payments

- School or college fees

- Transportation costs.

Types of Disability Insurance You Should Know

There are different types of disability coverage that are available. The right one depends on your job, your income and financial goals.

Short Term Disability Insurance – Quick Income Protection

Short-term Disability Coverage will provide income replacement for a short time that is usually 3 to 6 months and it also sometimes gives replacement up to one year. It is helpful if you face any minor surgeries, temporary illness, pregnancy related recovery or any short-term injuries. Short-term Disability Coverage usually start paying benefits after waiting period of 7 to 14 days

Long Term Disability Insurance – Long-Lasting Financial Security

Long-term disability coverage will provide benefits for a longer period. It can last for two years, five years, 10 years old even until the retirement age.

The plan is designed for serious injuries, chronic illness, permanent disability or long recovery periods. Long-term disability coverage usually starts after short-term benefit and or after waiting period of 60 to 180 days

Temporary Disability Insurance – Support During Recovery

Temporary disability coverage is very similar to short-term coverage. It provides income support for a limited time when you cannot work due to any temporary medical condition. There are some states and employers who are offering temporary Disability Coverage programs. These plans are useful for the short recovery periods.

Private Disability Insurance – Flexible Personal Protection

The private Disability Coverage is purchased directly from the insurance company. This plan is not provided by the government. This plan will give you more flexibility and better coverage options. You can also choose benefit amount, waiting period, benefit duration and additional riders. Private disability coverage is best for self-employed individuals or those who have stronger protection than employer coverage.

Individual Disability Insurance – Coverage That Moves With You

Individual Disability Coverage is a personal policy that belongs to you. Even if you change jobs, your coverage stays active as long as you are paying your premiums. This type of disability income insurance is perfect for doctors, lawyers, business owners and freelancers. And visual disability coverage offers customized protection that is based on your profession and your income level.

What Does Disability Insurance Really Cover?

Disability Coverage usually covers a percentage of your monthly income, a partial disability benefit, rehabilitation support and cost-of-living adjustment.

However disability coverage does not usually cover the injuries that are caused by illegal activities, self-inflicted injuries and pre-existing conditions in some cases. Make sure to always read your policy details very carefully before buying.

Powerful Disability Insurance Benefits – Explained

The main purpose of Disability Coverage benefits is income protection. But here are some of the key advantage

- The plan provide income replacement, you can continue to receive monthly payments if you cannot work

- It also gives financial stability, your family can continue paying the bills and maintaining their lifestyle

- It also gives peace of mind so you feel secure knowing your income is protected

- If you run a business the disability income insurance make sure that your personal finances stay safe

- It also gives flexible coverage options

Short vs Long Term Disability Insurance – Key Differences

Understanding the short and long term disability coverage will help you a lot to choose the right policy. Here we are discussing the key differences with the help of table.

| Feature | Short Term | Long Term |

| Duration | 3–12 months | 2 years to retirement |

| Waiting Period | 7–14 days | 60–180 days |

| Premium Cost | Lower | Higher |

| Best For | Temporary conditions | Serious long-term disabilities |

How Much Does Disability Insurance Cost?

The Disability Coverage cost depends on several factors. These factors are your age, your health condition, your occupation, income level, coverage amount, benefit. And also waiting period

On average the disability coverage can cost 1% to 3% of your annual income.

For example if you earn $50,000 per year, your premiums can be around $500-$1500 annually. Higher risk jobs can have higher premiums. Office workers usually pay less as compared to the construction workers.

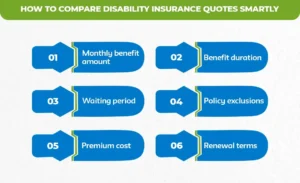

How to Compare Disability Insurance Quotes Smartly

Before buying a policy, always compare the Disability Coverage quotes from multiple providers. When reviewing the quotes, make sure follow

- Monthly benefit amount

- Benefit duration

- Waiting period

- Policy exclusions

- Premium cost

- Renewal terms

Who Actually Needs Disability Insurance?

There are so many people who think that disability insurance is only for the risk jobs. Well this is not true. You can’t need disability coverage if you

- Depend on your salary to pay bills

- You have children or family members who rely on you

- You have loans or mortgage payments

- You are self-employed

- You do not have large savings

Employer vs Individual Disability Coverage – What’s Better?

There are some employers who offer group disability insurance. This is helpful but it cannot be enough. Employer coverage can cover only 40% to 60% of income, it ends if you leave the job and also has limited customization.

While individual disability coverage can be fully portable, it gives you customized coverage and stronger income protection. For full protection, there are so many professionals who use private disability coverage in addition to employer benefits.

Must-Have Policy Features to Look For

Whenever you are choosing disability coverage, you have to look at these important features

- Own occupation vs any occupation

- Benefit period

- Waiting period

- Riders

Final Thoughts – Protect Your Income Before It’s Too Late

Disability coverage is one of the most important financial protection tools that is available today. Life insurance protects your family after death, while disability income insurance protects you while you are still alive. The goal is always the same, that is to protect your income and secure your future no matter if you choose short-term disability coverage , long-term disability coverage or the temporary one.

Before purchasing a policy, compare the disability coverage quotes, review the coverage carefully and choose a plan that fits your income and lifestyle. Protecting your income today means that you are protecting your tomorrow.

Not sure which plan is right for you?

Let M-life Insurance help you to compare the short term and long-term disability insurance options easily. Compare the plans today with our experts.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.