7 Key Facts About Borrowing Against Life Insurance

- You can only borrow against permanent life insurance

- Term life insurance does not allow borrowing

- The loan uses your policy’s cash value

- There is no credit check required

- Interest is charged on the loan amount

- Unpaid loans reduce your death benefit

- If not managed properly then your policy can lapse

There are so many people who ask if they borrow against life insurance or not? The answer is very simple and yes you can borrow but only in certain cases. Borrowing against life insurance can be a smart way to get quick cash without going through banks or credit checks. However it is very important to understand how it worked before you decide.

In this guide we will explain

- How to borrow against life insurance

- Which policies allow loans

- Can you borrow a case life insurance?

- The benefits and risks

- And some important things to remember.

Which Policies Let You Borrow Cash Value?

You can borrow against a life insurance policy, but only if it builds cash value. Here are the permanent policies that are providing cash value

- Whole life insurance

- Universal life insurance

- Variable life insurance

All these plans build cash value over time. The value acts like a savings account inside your policy. Once enough cash value has accumulated then you can borrow against it.

Can You Borrow Against Term Life Insurance? The Truth

No, the term life insurance does not build any cash value. It only provides coverage for a specific time that is 10, 20 or 30 years. Since there is no same company then there is nothing to borrow from. If your goal is to borrow a case life insurance in the future, you would need a permanent policy instead of the term coverage.

Borrow Against Whole Life Insurance: Everything Explained

If you have whole life insurance coverage, you can borrow a case whole life insurance once enough cash value has built up.

Whole life insurance guaranteed fixed premiums, guaranteed cash value growth and lifetime coverage.

Because of its steady growth, borrowing against the whole life insurance policy is common for emergencies, education expenses, medical bills or any other business expenses.

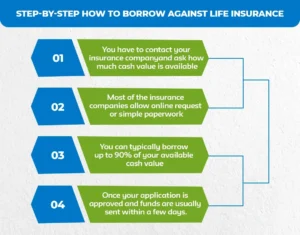

Step-by-Step: How to Borrow Against Life Insurance

If you qualify, then the process of borrowing life insurance is usually very simple.

- You have to contact your insurance company and ask how much cash value is available

- Most of the insurance companies allow online request or simple paperwork

- You can typically borrow up to 90% of your available cash value

- Once your application is approved and funds are usually sent within a few days.

How Borrowing Against a Life Insurance Policy Really Works

When you borrow against the life insurance policy, you are not withdrawing your money. Instead the insurance company gives you a loan using your cash value as a collateral

Here are some of the important things to understand

- interest will be charged on the loan

- You are not required to follow our strict repayment schedule

- If you do not repay then the loan plus interest will reduce your death benefit.

Let’s have a better understanding with an example

If your policy has a $200,000 death benefit and you borrow $30,000, your beneficiaries can receive $170,000 if the loan is not repaid.

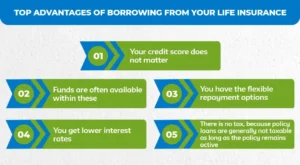

Top Advantages of Borrowing From Your Life Insurance

Borrowing against life insurance can offer so many benefits.

- Your credit score does not matter

- Funds are often available within these

- You have the flexible repayment options

- You get lower interest rates

- There is no tax, because policy loans are generally not taxable as long as the policy remains active

Risks and Pitfalls to Watch When Borrowing Against Life Insurance

Even though you can borrow against her life insurance or permanent life insurance policies, it is not always the best option. Here are some of the risks

- Unpaid loan reduced what your family will receive

- If unpaid interest can grow very quickly

- If the loan becomes larger than your cash values, the policy can cancel

- If the policy lapses with an outstanding loan then the loan amount could become taxable income

When Should You Consider Borrowing Against Life Insurance?

For against whole life insurance can make sense if you have a financial emergency, you need short term cash, you can’t avoid high interest or you have strong cash value build up.

The plan is not good if you cannot manage the interest, you are close to retirement and need full coverage and you have the other lower cost borrowing options.

How Much Can You Borrow From Your Policy?

Most of the insurance companies allow you to borrow 70% to 90% of your available cash value.

If your policy has $50,000 in cash value then you might be able to borrow $35,000-$45,000. But keep in mind that borrowing the maximum amount can increase the risk of policy labs

Repaying Your Life Insurance Loan: Tips and Tricks

The repayment option is very flexible. You can make the regular payments, pay only interest, pay in a lump sum or you choose not to repay. Even though the payment is very flexible, it is very smart to make a plan. This will protect your beneficiaries and keep your coverage active

Final Thoughts: Is Borrowing Against Life Insurance Right for You?

So yes, you can borrow but only if you have permanent coverage with cash value. Borrowing against life insurance can be very helpful in emergencies because it offers quick access to funds without credit checks. However it is not free money. Interest applies and unpaid loans also reduce your debt benefit. Always speak with the insurance provider all the financial advisor before making any decision.

If you need quick cash, see how M-life Insurance can help you to borrow safely. Talk with the expert today and get your problems solved.

FAQS

Is it a good idea to borrow against your life insurance?

It can be helpful if you need money quickly because you do not need a credit check. But be careful if you don’t pay it back, your money will reduce and your family will get less when you pass away.

What is the cash value of a $10,000 life insurance policy?

The cash value is the saving part of a permanent life insurance policy. For a $10,000 policy the cash value usually starts small in the first few years, maybe a few hundred dollars and close overtime. Term Life insurance does not have any cash value

How much money can I borrow from my life insurance policy?

You can borrow up to 70 to 90% of your policy’s cash value. For example if your policy has $9000 in cash value then you might be able to borrow $7000-$9000.

What is the cash value of a $250,000 life insurance policy?

The cash value depends on the type of policy you choose and how long you have had it. For a $250,000 permanent insurance policy the cash value you can grow to tens of thousands over several years. Term life insurance has no cash value at all.

Joyce Espinoza, Expert Life Insurance Agent

Joyce Espinoza is a trusted life insurance agent at mLifeInsurance.com. She’s been in the insurance industry for over ten years, helping people, especially those with special health conditions to find the right coverage. At MLife Insurance, Joyce writes easy-to-understand articles that help readers make smart choices about life insurance. Previously, she worked directly with clients at Mlife Insurance, advising nearly 3,000 of them on life insurance options.